Your royalty check is the end product of dozens of economic forces working all at once — and most of them have nothing to do with what’s happening on your property. In this episode, we break down the economic framework every mineral owner needs to understand: starting with the global or macro-economic forces that set the price of oil and gas, moving to the local and regional factors that determine how much of that price actually reaches your check, and ending with the micro or property-level decisions that affect your long-term income. Whether you inherited your minerals or actively manage them, understanding the big picture helps you make smarter decisions, set realistic expectations, and stop second-guessing every time your royalty check goes up or down.

Be sure to also subscribe on Apple Podcasts via the link above and please leave us an honest rating and review. We read every one of them and sincerely appreciate any feedback you have. To ask us a question to be featured on an upcoming episode, please leave a comment below or send an email to feedback@mineralrightspodcast.com.

Global Supply & Demand: The Foundation of Every Royalty Check

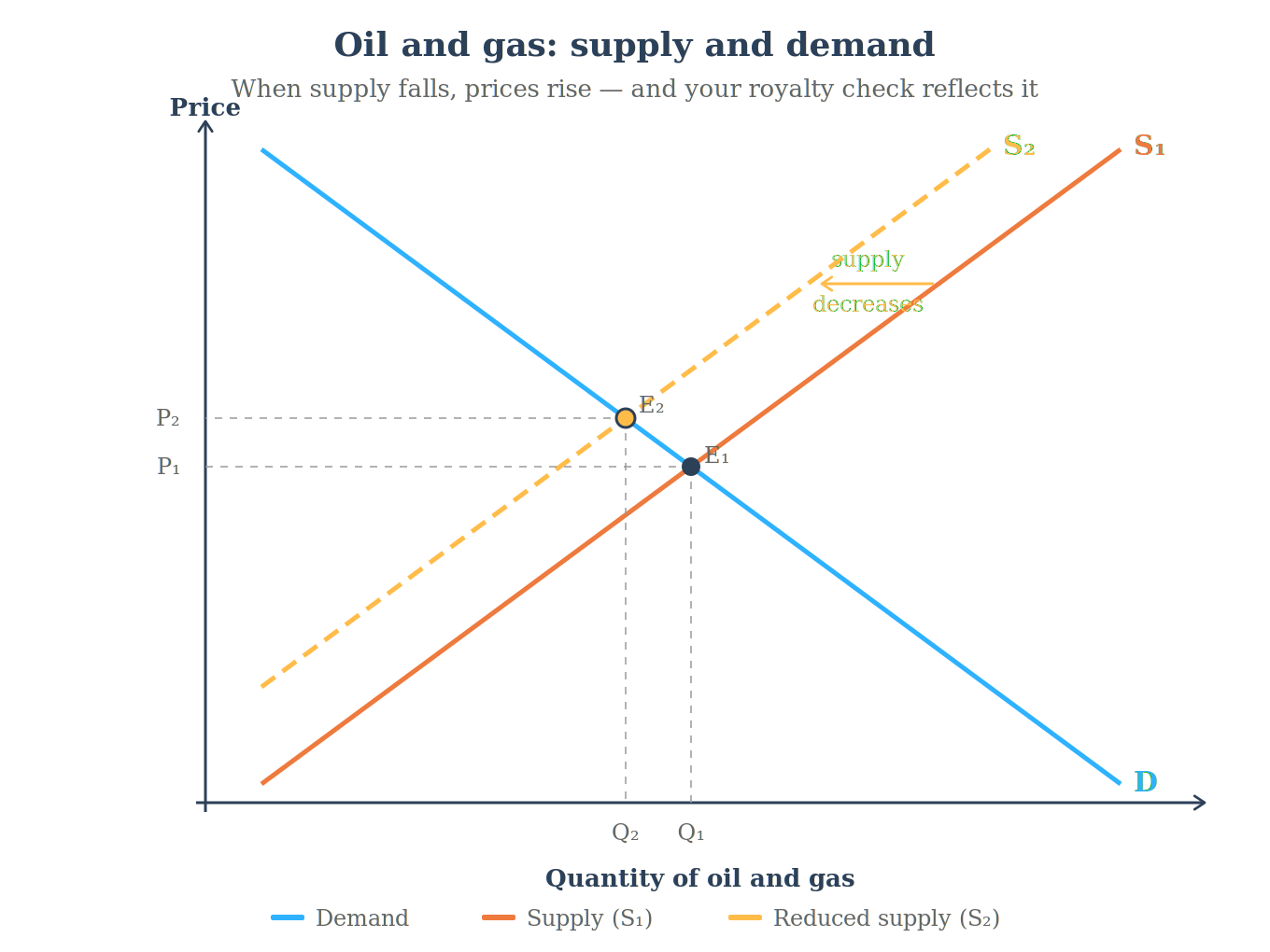

Oil and gas are priced in a global marketplace, and at the most basic level, the same rules apply as any other market: when more buyers want oil or gas than sellers have available, prices go up; when supply floods the market, prices fall. Economic growth is one of the most powerful demand drivers — a growing global economy means more shipping, more industrial activity, more energy consumption, which leads to higher demand for oil and gas (and typically higher royalty income).

One important thing to understand about oil and gas is that demand is what economists call “inelastic.” That means people and industries don’t significantly cut their consumption just because prices rise. For example, we still need to heat our homes or drive to work and will make adjustments to meet those needs first. Whether oil is $60 a barrel or $120 a barrel, demand for gasoline, diesel, jet fuel, and heating fuel remains largely intact — which provides a natural floor under prices over time. The flip side is also true: when the global economy contracts, as it did during COVID-19 and the ensuing oil price war, demand can crater quickly and prices can fall just as fast.

OPEC and the Rise of U.S. Production

OPEC has historically controlled oil prices by adjusting how much member countries produce. When Saudi Arabia and other member nations decide to “close the spigot,” global supply tightens and prices rise. When they flood the market, prices fall (at least historically that was true). And it’s not just current supply and demand that matters — oil prices are influenced heavily by expectations of future supply and demand, which is why trader sentiment and the futures market can move prices before a single barrel changes hands.

What has changed significantly over the past decade is the rise of the United States as the world’s largest crude oil producer. That shift has meaningfully reduced OPEC’s ability to dictate prices — their decisions simply don’t move the needle the way they once did. The COVID-era price crash was a vivid case study: demand cratered due to lockdowns, and Saudi Arabia simultaneously flooded the market to squeeze U.S. shale producers, briefly pushing the price of oil below zero for the first time in history. The companies that survived that period came out leaner and more disciplined, which makes a repeat of that scenario less likely going forward.

Today, the U.S. position as the dominant global producer acts as a buffer. During the April 2026 Iran conflict, oil prices would likely be trading far higher if U.S. production weren’t providing a counter-balance to the supply disruption.

Geopolitics, Weather, and the Risk Premium

Oil markets don’t just react to disruptions — they anticipate them. The “risk premium” is the extra cushion that traders build into oil and gas prices when there’s a credible threat of a future supply disruption, even if nothing has actually happened yet.

A good way to watch this in action: the next time a named storm enters the Gulf of Mexico during hurricane season, watch what the price of crude oil does in the days before it makes landfall. It’ll tick up as traders price in the possibility of production shutdowns. And if the storm turns out to be less damaging than feared, prices will often drop back — sometimes below where they started — as that risk premium unwinds.

Geopolitical events like the 2026 Iran conflict, military actions that threaten shipping lanes, or sanctions on major producing nations all create the same kind of uncertainty. These forces can move your royalty income without any change in your own wells or your operator’s behavior. Nobody can perfectly predict these moves — if they could, they’d be a trillionaire.

Sanctions and Government Actions as a Market Force

Beyond weather and conflict, governments believe they have a powerful tool for disrupting commodity markets: economic sanctions. When the U.S. or its allies restrict a major oil-producing nation’s ability to sell into global markets (as with Russia as a result of invading Ukraine), they are attempting to engineer a supply reduction — and supply reductions tend to push prices up.

The three big examples that mineral owners should be aware of are Iran, Russia, and Venezuela. At various points, sanctions have targeted the oil exports of all three, affecting anywhere from 1 to 5 million barrels per day of supply. The nuanced reality is that markets adapt — sanctioned oil tends to get rerouted to China and other buyers rather than simply disappearing. That rerouting adds friction and cost to global supply chains, but it limits the direct price impact on benchmark crude.

The policy lever cuts both ways. When the U.S. signals it may ease sanctions to relieve supply tightness — as happened with Venezuela during the Iran conflict in 2026 — it can help cap price spikes. Tightening sanctions on a new target, on the other hand, can cause a short-term supply shock that may take some time before those volumes find their way into the market. The important thing to remember is that geopolitics and weather are outside any mineral owner’s control.

Natural Gas: A Different Market With Different Rules

Natural gas is not the same market as crude oil, and it’s important to understand that distinction. It’s harder to transport, far more regional in nature, and priced at a different benchmark — the Henry Hub, a physical pipeline interconnection in Louisiana that serves as the national reference price for domestic gas.

Natural gas prices are driven heavily by storage inventory levels. When there’s a surprise draw-down from storage — gas being consumed faster than expected — prices can spike quickly. And gas tends to be more sensitive to seasonal weather than oil is. A warm winter can tank gas prices just as fast as a geopolitical event can spike oil prices, and the two commodities don’t necessarily move together.

What has changed the picture meaningfully in recent years is the growth of LNG (liquefied natural gas) exports. The ability to ship U.S. natural gas overseas in liquid form has introduced global demand that didn’t exist a decade ago. Europe’s need to replace Russian supply and Asia’s growing appetite for U.S. gas now help put a floor under domestic prices. A warm winter that would have once crushed the Henry Hub benchmark price for natural gas doesn’t hurt as badly when overseas buyers are absorbing some of the excess supply.

Basis Differentials: Why Your Local Price Is Not the Benchmark Price

Here’s something that surprises a lot of mineral owners when they first encounter it: the price you see reported for WTI crude oil or Henry Hub natural gas is not necessarily what your operator is getting paid for production from your property. It’s a benchmark price at a specific trading location — Cushing, Oklahoma for oil, Louisiana for gas. What actually gets paid at your wellhead can be significantly different, and that gap is called the basis differential.

Two things primarily drive the differential. The first is quality. Heavier, sulfur-rich “sour” crude sells at a discount to light, sweet WTI, which is easier to refine and more widely in demand. The second — and often larger — factor is transportation cost and infrastructure. The further or harder it is to get oil or gas to market, the lower the local price. Getting a commodity to a buyer costs money, and someone has to absorb that cost.

Here’s an analogy: imagine you grow apples in a remote valley with only one road out. If that road gets washed out, you can’t get your apples to market — you either sell them cheap locally or not at all (and risk that they will spoil). Mineral owners face a similar dynamic when pipeline capacity is limited or nonexistent in their area.

A real-world example of how severe this can get: crude oil produced in the Uinta Basin in Utah is so thick and waxy at room temperature that it literally solidifies at ambient temperature and can’t be pumped through a standard pipeline. It has to be transported by railcar, which adds substantial cost and consistently results in a realized price $10 or more per barrel below WTI.

Regardless of where your minerals are located, even two operators sitting side by side on the same formation can end up receiving different prices for their production, depending on the purchase contracts and hedging arrangements each has in place.

The practical takeaway is simple: always look at the actual “realized price” on your royalty statement rather than the benchmark you see in the news. If there’s a significant gap, it’s usually explained by the local basis differential, quality adjustments, and post-production deductions — not necessarily something your operator is doing wrong.

The Waha Hub: When Infrastructure Falls Behind Production

The Waha Hub in West Texas is the most dramatic recent example of a basis differential becoming extreme — and it offers a powerful lesson for anyone who owns mineral rights in the Permian Basin.

Most of the natural gas produced in West Texas comes out of the ground as “associated gas” — a byproduct of oil production. Operators are drilling for oil, and the gas comes along with it whether they want it or not. Over a five-year period, natural gas production in the Permian more than doubled. The problem is that pipeline takeaway capacity hasn’t kept pace, which means there’s more gas being produced than there are pipelines to carry it away.

The result: Waha Hub gas prices have gone negative. Meaning operators are effectively paying companies to take the gas off their hands because there’s no other option. On days when the Henry Hub benchmark is at $3.00 per thousand cubic feet, Waha has traded at negative $5.00 — a differential of $8.00 that flows directly through to royalty owners as near-zero or negative revenue on the gas line of their check.

The numbers tell the story clearly. Waha prices first went negative in 2019, happened 49 times in 2024, and by early 2026 had been negative for a record 25 consecutive days, reaching as low as negative $7.15 per MMBtu in a single session. The total royalty check doesn’t go negative because the oil revenue offsets the gas — but if you own gas-heavy minerals in the Permian, this is a very real risk.

One emerging response is to bring the market to the source rather than build pipelines to take gas somewhere else. Bitcoin mining operations and AI data centers are being built in West Texas specifically to consume cheap stranded gas at the wellhead — a creative solution, but one that underscores how significant the infrastructure gap has become. New pipelines are under construction, but analysts caution that relief may be temporary if Permian production continues growing at its current pace.

Well Potential and Geology: What’s Actually Under the Ground

Once you move past global prices and local infrastructure, the next layer of value comes down to your specific property — and it starts with geology. The most fundamental question in mineral rights value is: what can this property realistically produce, both now and in the future?

Not all acres in a basin are equal. Properties in the proven “sweet spot” of a formation can be worth dramatically more than acreage on the fringe of the same play, even with identical royalty rates and acreage size. Reservoir quality, well length, and the number of future well locations a property can support all factor into how much that property is ultimately worth.

A practical way to get a sense of what your undrilled property might produce: look up production data from offset wells — wells already drilled near your minerals in the same formation — using your state’s oil and gas commission website. That data is publicly available and gives you the most realistic picture of what development might look like on your property.

Decline Curves: Why Your First Check Is Not Your Normal Check

Shale wells don’t produce at a constant rate — they start high and decline steeply, then gradually flatten out over time. It’s completely normal to see production fall 50–70% within the first 12 to 18 months. That first royalty check can look like a windfall, but basing spending decisions on it is a mistake that catches a lot of new royalty owners off guard.

The important thing is to understand this behavior in advance so you’re not shocked when the check drops — and so you don’t mistake normal decline for something being wrong. A declining check is expected. What isn’t expected, and what should prompt a closer look, is production that suddenly drops to zero and stays there. That can indicate a mechanical or operational problem worth investigating with your operator.

When it comes to budgeting, use the more stable mid-life production levels — months 12 through 24 and beyond — as your baseline. Those numbers are a far more sustainable guide to what your property will generate on an ongoing basis.

The Royalty Rate: The One Lever You Actually Control

Almost everything discussed in this episode is outside a mineral owner’s control. Global commodity prices, local basis differentials, geology, and well production rates are all things that happen to you rather than things you can influence. But the royalty rate is different — it’s the one variable you can actually negotiate, and it’s the most powerful lever available to you.

The royalty rate is the percentage of gross production revenue you receive from any well drilled on your land. It’s set at leasing and locked in for the life of the lease, which means the decision you make at the negotiating table compounds across every barrel of oil and every cubic foot of gas produced — for every well drilled, for the life of the property.

The math matters more than it might appear. Negotiating from a 3/16 royalty (18.75%) to a 1/4 royalty (25%) doesn’t just mean a slightly larger check each month. It means your property is worth approximately 33% more to any buyer, because buyers are paying for the income stream the royalty rate will generate over the life of all the wells. That’s a 33% increase in value for a negotiation that costs you nothing except the effort to ask.

Every mineral owner, regardless of how few acres they hold, has the ability to negotiate for a higher royalty rate. It is worth the effort almost every time, even if it means a lower upfront lease bonus.

Time Value of Money: When You Get Paid Matters as Much as How Much

The last piece of the economic framework is the concept of time — and specifically, the idea that a dollar received today is worth more than a dollar promised in the future. This isn’t just a financial theory; it has very practical implications for how mineral rights are valued and how you think about your own property.

There are three reasons future money is worth less than present money. First, inflation erodes purchasing power over time — a dollar will buy less ten years from now than it does today. Second, money received today can be invested and grow; a dollar sitting in the future hasn’t been put to work yet. Third, future payments carry uncertainty that today’s payments don’t. A well could stop producing, commodity prices could collapse, or an operator could delay development — and the further out in time that payment is, the more likely it is that something interferes.

For undeveloped mineral rights, the timing question is one of the biggest drivers of value. A property where a well is being drilled today is worth far more than an otherwise identical property where drilling is five years away — even if the geology is exactly the same and the eventual production will be exactly the same. The buyer knows that the earlier cash flow is worth more.

One lever mineral owners can sometimes negotiate is continuous drilling provisions in a lease, which require the operator to stay on a development schedule rather than sitting on your acreage indefinitely. Bringing forward the timing of drilling is the same as increasing the present value of your property.

There’s also a practical connection to commodity prices: when oil prices are high and operators are actively drilling, it’s the ideal time to lease — because operators are motivated to drill quickly, which improves your negotiating position and pulls your royalty income forward in time. When prices are low and operators are in no hurry, your wait gets longer and the present value of your future royalties goes down.

Putting It All Together

Macro, micro, and time all interact simultaneously — which is exactly what makes valuing mineral rights and royalties so complex. A property in West Texas with strong geology and a high royalty rate might still generate disappointing income if Waha Hub gas prices are deeply negative and oil prices have softened. A property in an active drilling area with a rig on location might be worth far more than identical acreage that won’t see a well for a decade.

Understanding these layers doesn’t require an economics degree. It just requires knowing what questions to ask when you read a news article about oil prices, pipeline maintenance, or a geopolitical event. Because now you can ask: how does this affect my local pricing? When is the next well expected on my property? What is my royalty rate, and am I getting the most out of it? Those questions put you in the driver’s seat as a mineral owner and the answers will help you make the most of your minerals and royalties.

Resources

- MRP Episode 4: How Mineral Rights Are Valued

- MRP Episode 194: Calculating Mineral Rights Value (Deeper Dive)

- My Mineral Management Basics Course — the recommended starting point for understanding your property, finding key documents, and researching nearby well production

- EIA: What Drives Crude Oil Prices

- EIA: Henry Hub Natural Gas Spot Price History

- EIA: The Waha Hub Natural Gas Price and Henry Hub Differential

- NARO Membership (use code MRPODCAST for a $25 discount for new Introductory Members)

Thanks for Listening!

To share your thoughts:

- Leave a comment or question below (we read each one and your question may be featured in a future episode)!

- Ask a question or leave us feedback via email.

To help out the show:

Click the Apple Podcasts Logo Above to leave us a rating & review. It really helps us reach those that need to hear this information and only takes a minute. We greatly appreciate it! Plus, you can get a shout out on a future episode!

Thanks again – until next time!

Disclaimer: This episode and accompanying show notes are provided for general information purposes and should not be construed as financial, legal, or investment advice. For guidance specific to your situation, please consult with a qualified attorney, CPA, or financial advisor.

{kind=link}